via TechRadar - All the latest technology news http://bit.ly/2UFAgOO

Good news: Apple now allows you to download bigger apps over a cellular connection than it used to.

Bad news: there’s still a cap, and you still can’t bypass it.

As noticed by 9to5Mac, the iOS App Store now lets you download apps up to 200 MB in size while on a cell network; anything bigger than that, and you’ll need to connect to WiFi. Before this change, the cap was 150 MB.

And if you’ve got an unlimited (be it actually unlimited or cough-cough-‘unlimited’) plan, or if you know you’ve got enough monthly data left to cover a big download, or you just really, really need a certain big app and WiFi just isn’t available? You’re still out of luck. That 200 MB cap hits everyone. People have found tricky, fleeting workarounds to bypass the cap over the years, but there’s no official “Yeah, yeah, the app is huge, I know.” button to click or power user setting to toggle.

The App Store being cautious about file size isn’t inherently a bad thing; with many users only getting an allotment of a couple gigs a month, a few accidental downloads over the cell networks can eat up that data quick. But it really does suck to open up an app you need and find it’s requiring some update that exceeds the cap, only to realize you’re nowhere near a friendly WiFi network. At least give us the choice, you know?

On the upside, most developers seem to be pretty aware of the cap; they’ll hack and slash their app install package until it squeaks under the limit, even if it means downloading more stuff through the app itself post-install. Now, at least, they’ve got 50 more megabytes of wiggle room to start with.

Tesla’s big bet on China-based production is key to a new effort to lure Chinese consumers with cheaper prices. Today the U.S. firm revealed that its incoming Model 3, which will be produced in China, will sell from 328,000 RMB — that’s around $47,500 and some 13 percent cheaper than its previous entry-level option.

The company opened pre-orders for the vehicle today, although it only broke ground on its Shanghai-based factory in January of this year. Customers who do plonk down cash for a pre-order this week — deposits start from 20,000 RM — can expect to receive their vehicle in 6-10 months, according to Tesla.

Despite the competitive prices, the higher spec Model 3 will continue to be shipped from the U.S, according to Reuters. The publication added that it isn’t clear if the made-in-China Tesla will qualify for EV subsidies from the government.

Beyond China, the Model 3 also went up for pre-order in Australia, Hong Kong, Japan, New Zealand, Ireland and Macau, the company said.

The Shanghai plant is expected to produce 500,000 vehicles per year when it reaches full production. The factory began hiring workers this month after job listings were published online, while videos and photos of the factory taken by Tesla enthusiasts suggest that it is nearing completion.

While it isn’t clear what margins the China-produced vehicles will bring Tesla, local manufacturing will help it avoid challenges around shipping and pricing, an issue that has been exacerbated by the ongoing U.S-China trade war.

Foursquare just made its first acquisition. The location tech company has acquired Placed from Snap Inc on the heels of a fresh $150 million investment led by the Raine Group. The terms of the deal were not disclosed. Placed founder and CEO David Shim will become President of Foursquare.

Placed is the biggest competitor to Foursquare’s Attribution product, which allows brands to track the physical impact (foot traffic to store) of a digital campaign or ad. Up until now, Placed and Attribution by Foursquare combined have measured over $3 billion in ad-to-store visits.

Placed launched in 2011 and raised $13.4 million (according to Crunchbase) before being acquired by Snap Inc. in 2017.

As part of the deal with Foursquare, the company’s Attribution product will henceforth be known as Placed powered by Foursquare. The acquisition also means that Placed powered by Foursquare will have more than 450 measureable media partners, including Twitter, Snap, Pandora, and Waze. Moreover, more than 50 percent of the Fortune 100 are partnered with Placed or Foursquare.

It’s also worth noting that this latest investment of $150 million is the biggest financing round for Foursquare ever, and comes following a $33 million Series F last year.

Here’s what Foursquare CEO Jeff Glueck had to say about the financing in a prepared statement:

This is one of the largest investments ever in the location tech space. The investment will fund our acquisition and also capitalize us for our increased R&D and expansion plans, allowing us to focus on our mission to build the world’s most trusted, independent location technology platform.

That last bit, about an independent location technology platform, is important here. Foursquare is ten years old and has transformed from a consumer-facing location check-in app — a game, really — into a location analytics and development platform.

Indeed, when Glueck paints his vision for the company, he lists five key areas of focus:

You’ll notice that its consumer apps, Foursquare and Swarm, are at the bottom of the list. But that’s because Foursquare’s real technological and strategic advantage isn’t in building the best social platform. In fact, Glueck said that more than 90 percent of the company’s revenue came from the enterprise side of the business. Foursquare’s advantage is in the accuracy of its technology, as afforded by the decade of data that has come from Foursquare, Swarm, and the users who have expressly verified their location.

The Pilgrim SDK fits into that top item on the list: developer tools. The Pilgrim SDK allows developers to embed location-smart experiences and notifications into their apps and services. But it also expands Foursquare’s access to data from beyond its own apps to the greater ecosystem, yielding the data it needs to power analytics tools for brands and publishers.

With this acquisition, Placed will be able to leverage Foursquare’s existing map of 105 million places of interest across 190 countries, as well as tap into the measured U.S. audience of over 100 million monthly devices.

Foursquare and Placed share a similar philosophy of building against a truth set of real consumer responses. Getting real people to confirm the name of their location is the only way to know if your technology is accurate or not. Placed has leveraged over 135 million survey responses in its first-party Placed survey apps, all from consumers opted-in to its rewards app. Foursquare expands the truth set for machine learning exponentially by adding in our over 13 billion consumer confirmations.

The hope is that Foursquare is accurate enough to become the de facto location analytics and services company for measuring ad spend. With enough scale, that may allow the company to break into the walled gardens where most of that ad spend is going, Facebook and Google.

Of course, to win as the “world’s most trusted, independent location technology platform,” consumers have to trust the platform. After all, one’s location may be the most sensitive piece of data about them. Foursquare has taken steps to be clear about what its technology is capable of. In fact, at SXSW this year, Foursquare offered a limited run of a product called Hypertrending, which was essentially an anonymized view of real-time location data showing activity in the Austin area.

Here’s what Chairman of the Board and cofounder Dennis Crowley had to say at the time:

We feel the general trend with internet and technology companies these days has been to keep giving users a more and more personalized (albeit opaquely personalized) view of the world, while the companies that create these feeds keep the broad “God View” to themselves. Hypertrending is one example of how we can take Foursquare’s aggregate view of the world and make it available to the users who make it what it is. This is what we mean when we talk about “transparency” – we want to be honest, in public, about what our technology can do, how it works, and the specific design decisions we made in creating it.

With regards to today’s acquisition of Placed, Jeff Glueck had this to say:

Both companies also share a commitment to privacy and consumers being in control. Our Foursquare credo of “data as a privilege” only deepens as our company expands. We believe location should only be shared when consumers can see real value and visible benefits driven by location. We remain dedicated to elevating the industry through respect for transparency, user control, and instituting layers of privacy safeguards.

This new financing brings Foursquare’s total funding to $390.4 million.

The company sought to completely change how we interacted with computers, but now Leap Motion is selling itself off.

Apple reportedly tried to get their hands on the hand-tracking tech which Leap Motion rebuffed, but now the hyped nine-year-old consumer startup is being absorbed into the younger, enterprise-focused UltraHaptics. The Wall Street Journal first reported the deal this morning, we’ve heard the same from a source familiar with the deal.

The report further detailed that the purchase price was a paltry $30 million, nearly one-tenth of the company’s most recent valuation. CEO Michael Buckwald will also not be staying on with the company post-acquisition, we’ve learned.

Leap Motion raised nearly $94 million off of their mind-bending demos of their hand-tracking technology, but they were ultimately unable to ever zero in a customer base that could sustain them. Even as the company pivoted into the niche VR industry, the startup remained a problem in search of a solution.

In 2011 when we first covered the startup, then called OcuSpec, it had raised $1.3 million in seed funding from Andreesen Horowitz and Founders Fund. At the time, Buckwald told us that he was building motion-sensing tech that was “radically more powerful and affordable than anything currently available” though he kept many details under wraps.

As the company first began to showcase its tech publicly, an unsustainable amount of hype began to build for the pre-launch module device that promised to replace the keyboard and mouse for a PC. The device was just a hub of infrared cameras, the magic was in the software which could build skeletal models of a user’s hands and fingers with precision. Leap Motion’s demos continued to impress, the team landed a $12.8 million Series A in 2012 and went on to raise a $30 million Series B the next year.

In 2013, we talked with an ambitious Buckwald as the company geared up to ship their consumer product the next year.

The launch didn’t go well as planned for Leap Motion, which sold 500,000 of the modules to consumers. The device was hampered by poor developer support and a poorly unified control system, in the aftermath the company laid off a chunk of employees and began to more seriously focus its efforts on becoming the main input for virtual reality and augmented reality headsets.

Leap Motion nabbed $50 million in 2017 after having pivoted wholly to virtual reality.

The company began building its own AR headset all while it was continuing to hock tech to headset OEMs, but at that point the company was burning through cash and losing its lifelines.

The company’s sale to UltraHaptics, a startup that has long been utilizing Leap Motion’s tech to integrate its ultrasonic haptic feedback solution, really just represents what a poor job Leap Motion did isolating their customer base and its unwillingness to turn away from consumer markets.

Hand-tracking may still end up changing how we interact with our computers and devices, but Leap Motion and its later investors won’t benefit from blazing that trail.

If you’re a cannabis investor or a founder working on a cannabis-related startup, you’ve probably heard of Poseidon Asset Management.

The San Francisco-based investment firm is one of very few that is focused narrowly on the industry, which remains fairly insular for now. Poseidon has also been at it longer than most outfits, having begun making bets on cannabis-related companies six years ago. More, Poseidon has managed to stuff checks into some of the fastest-growing companies in the sector, including the cannabis vaporizer company Pax Labs and the e-cigarette company Juul, whose founders created the Pax vaporizer before peeling off to win over smokers. Indeed, because Poseidon has largely invested the money of high-net-worth individuals and family offices, it hasn’t been constrained by the same vice clauses — or restrictions by backers like pension funds and other institutions — that can impact where venture capitalists invest.

Poseidon is notable for yet another reason, too. It was founded by siblings Emily and Morgan Paxhia, whose parents both died of different cancers at the ages of 46 and 52, respectively. In fact, despite — or because of — being a young teenager at the time, Emily Paxhia says she can still very much remember the hospice nurse who recommended to her father that he smoke pot to ease his pain. Little did Paxhia know then that cannabis — then a surprising and exotic concept — would later inform the career she now enjoys.

We talked about it earlier this week, as well as how Paxhia and her brother decided back in 2013 that cannabis was going to be the next big thing. If you’re curious about their path, and where they’re shopping now, read on.

TC: You grew up in Buffalo and you say your parents were entrepreneurial.

EP: Our dad restored homes in an economically depressed part of Buffalo, and our mom worked for a real estate agency. When she began running his books, voilà, we had a family business.

TC: Then he became sick when you and your siblings were young. How did that impact you?

EP: He was a dyed-in-the-wool hippy. We had Woodstock tickets in our home. He never really accepted the status quo, which I think informs the way we view the world. But yes, he became aggressively sick with cancer in 1994 and passed away in 1996, and it was this non-virtuous cycle, where they would put him on this or that medication and each had its own terrible side effects. Finally, a hospice nurse who came to our home said, “John, maybe you should smoke some pot.” She told us it would help with his appetite and reduce his anxiety and help him sleep. It was this palliative care thing that had been stigmatized but she believed was useful. I don’t know if he tried it or not, but then he passed away, and five years later, our mother, who was very healthy and ran and took care of herself, also died of cancer.

I’ve often looked back and thought that if my parents had [used cannabis at the end of their lives], they would not have suffered so greatly.

TC: How did you get from Buffalo to starting a fund in San Francisco, seemingly out of the blue?

EP: After college, I was spending time in New York and in San Francisco, working in market research, including on behalf of Amex and Viacom and Comedy Central — all companies competing in markets that were very saturated. It was hard to find white space. When I moved to California, I started to see people lining up outside the doors of dispensaries and I thought, Here are people who ordinarily wouldn’t break a law, but they’re doing something that’s federally illegal because they want cannabis. Brick-and-mortar is dying elsewhere and it’s thriving here. This is what product-market fit looks like.

TC: At what point did you decide to partner with your brother and why?

EP: He worked for UBS during the downturn [of 2008] and then he landed in Rhode Island, working for a private registered investment advisor. And I called him, and I said, “Dude, I think the ‘thing’ of our generation is cannabis.” I actually remember where I was standing in San Francisco. We’d always thought we’d be in business together, and he took me 100% seriously, and then we couldn’t turn it off. From that point on we were figuring out how do we participate in this?

It was Morgan who identified that a fund made the most sense, that the industry was happening and it was very underserved from a tech and investor perspective. He knew the industry was going to need funding and that investors would need an actively managed strategy.

TC: How did you get started?

EP: It was hard. It was very hard to find attorneys to work with us, but we did. The same was true of auditors and back-office administration. Everything that’s normally a check-the-box type of process was hard.

TC: What about investors? How did you begin lining these up without a track record?

EP: I had that qualitative consulting experience, working with brands and helping them scale; Morgan had traditional investment experience. But there were no data sets at the time. All we could do was be “in market” all the time. We traveled to be with companies. We traveled to different geographies because each has such complicated regulatory nuances to it.

Raising money was really difficult. We got laughed at quite a bit. It’s funny, many of our earliest investors were lawyers because I think they understood the real, versus the perceived, risk involved in what we were doing.

TC: Eventually, you began to assemble this evergreen-type fund and you began investing while fundraising. Where were you shopping at the outset?

EP: We focused initially on the tech aspect of the industry. To us, that was where we saw the biggest gap and the biggest opportunity to potentially scale quickly. Also, those companies tended to be started by tech founders who were [secondarily] interested in cannabis.

TC: How were you drumming up deal flow?

EP: It was going into stores, seeing what they were using in terms of tech, talking with retail associates about what people were buying, going to industry events and to cannabis job fairs to see who was hiring, then starting to build relationships with those companies. We knew as entrepreneurs ourselves that being as founder-friendly as possible would be the key to our deal flow. And we started having founders bringing us other founders. We’ve now led 20 rounds at this point, and our best deal flow has come from the founders themselves.

But it’s also been a matter of getting out there and walking up to people and saying, “Have you thought about raising capital? If so, let’s keep talking.”

TC: Do you feel like you now recognize founders you shouldn’t back?

EP: What 100% does not work in this industry is hubris. In other areas of business, a certain level of confidence bodes well for founders. But this is not a move-fast-and-break-things industry. There are so many regulatory challenges that you really need to know the lay of the land. I’ve seen people come in and bounce right out again because of their attitude.

Founders also need to understand the extra costs in time and money that come with running these businesses and to model accordingly; otherwise, projections are off and valuations are off and you’re potentially facing a down round later in time.

TC: You were able to return money to investors in January, after Juul distributed a special dividend. Is that your biggest exit to date?

EP: That was a big one, but we’ve had other big exits out of [an earlier] pair of funds through [several investments in Canadian companies], including [medical marijuana company] Aphria [which went public last October] and Canopy Growth [which went public in 2014, is Canada’s second-largest grower and is currently valued at roughly $15 billion]. Canada is a very different market. You can order cannabis from the government and it will arrive in the postal mail. It’s very top-down unlike in the U.S., where the market is very bottom-up and state by state.

There’s a lot of investment going on [across U.S. and Canada]. It’s very permeable at this point. I was in Toronto last week, and licensed producers there want to invest more in California. We’re meanwhile looking at Latin America and Europe.

TC: That’s interesting. Where in Latin America and why?

EP: The cost to produce cannabis in Colombia is extremely low. Cannabis grows on a 12-hour cycle very well and the equator runs through the country’s southern sector [making its warm climate conducive to the plant’s growth]. Local companies can export the products at a lower cost than in Canada and Europe. [Operators there] also have distribution relationships with European markets [that are buying medical marijuana].

Mexico is also expected to roll out its medical program in the fourth quarter of this year, which is exciting.

TC: Obviously these places have been home to drug cartels for years. Do you worry that these same organizations will take an interest in what’s being built legally in their backyards?

EP: We’ve gotten comfortable with both places. I think the cartels have begun to pivot to other places like meth. I also don’t think it’s worth it to the cartels to get involved with legal government channels. And the groups that we focus on are themselves focused on medical cannabis and distribution to other medical touch points globally [and not the same places into which cartels are trying to move goods].

TC: I’ve read that Poseidon is trying to raise a new, $75 million fund. How far along are you?

EP: We have capital commitments for half the fund and hope to close it this summer. We want to be able to deploy [more capital] before legalization is [more widespread] and we have to compete with bigger funds.

TC: What is your pacing like? Relatedly, how fast do you have to move on these investments, or do you have all the time in the world right now?

EP: We expect to invest this new fund in 15 companies over two years. We’ve funded five startups with it since November, but we were in diligence on one of those for months. I’d say the average deal takes 60 to 90 days to pull together right now. We start our own diligence before the company is considering a Series A, which is where we invest. We want to help structure the round, to lead it, to have a board seat — to demonstrate our value add.

TC: Are you seeing many, or any, particularly frothy deals?

EP: Valuations are not going crazy, but the more popular a deal gets, the harder it becomes, as with any investment. We’re wrestling over a term sheet right now because other groups got a look at it and want us to lead it, but we’re also getting negotiated against a little bit.

TC: Any parting words for investors who want to jump into the industry? Any advice?

EP: I’d say to go to events and walk the floor to see who and what stands out.

I went to MJBizCon [the Marijuana Business Conference and Expo] that happens annually every winter. The first few years that we went, there were a few hundred schlubby guys walking the floor. The year before last, there were 3,000 people in attendance, looking a lot less schlubby. Last year, I think there were 27,000 people, which I took as an indicator that there’s some interest in this space. [Laughs.]

Amazon’s behavior toward open source combined with lack of leadership from industry associations such as the Open Source Initiative (OSI) will stifle open-source innovation and make commercial open source less viable.

The result will be more software becoming proprietary and closed-source to protect itself against AWS, widespread license proliferation (a dozen companies changed their licenses in 2018) and open-source licenses giving way to a new category of licenses, called source-available licenses.

Don’t get me wrong — there will still be open source, lots and lots of it. But authors of open-source infrastructure software will put their interesting features in their “enterprise” versions if we as an industry cannot solve the Amazon problem.

Unfortunately, the dark cloud on the horizon I wrote about back in November has drifted closer. Amazon has exhibited three particularly offensive and aggressive behaviors toward open source:

Amazon’s behavior toward open source is self-interested and rational. Amazon is playing by the rules of what software licenses allow. But these behaviors and their undesirable results could be curbed if industry associations created standard open-source licenses that allowed authors of open-source software to express a simple concept:

“I do not want my open-source code run as a commercial service.”

Leadership often comes from unexpected sources.

But the OSI, an organization that opines on the open-sourceness of licenses, is an ineffective wonk tank that refuses to acknowledge the problem and insists that unless Amazon has the “freedom” to take your code, run it as a commercial service and give nothing back to you, your code is not “open source.” The OSI believes it owns the definition of open source and refuses to update the definition of open source, which is short-sighted and dangerous.

To illustrate: The Server Side Public License (SSPL) — the license proposal spearheaded by MongoDB — was patterned exactly after the Gnu General Public License (GPL) and the Affero General Public License (AGPL). SSPL is a perfectly serviceable open-source license, and like GPL and AGPL, rather than prohibit software from being run as a service, SSPL requires that you open-source all programs that you use to make the software available as a service.

A months-long comical debate ensued after SSPL was proposed as an open-source license candidate to OSI, after which OSI made its premeditated opinion official, that SSPL is not an open-source license, even though GPL and AGPL are open source. In its myopia, the OSI forgot to be consistent: If SSPL is not open source, then GPL and AGPL should not be either. MongoDB will continue to use SSPL anyway, but it just won’t be called “open source” because OSI says that it owns the definition of “open source” and it can’t be called that. Great.

Is it inevitable that the combination of Amazon’s behavior and this lack of industry leadership will stifle open-source innovation and make commercial open source less viable? Should we just live with either more software becoming proprietary and closed-source to protect itself against AWS, or with widespread license proliferation?

We’ve already seen plenty of license proliferation. MongoDB SSPL, Confluent Community License (CCL), Timescale License (TSL), Redis Source Available License (RSAL), Neo4J Commons Clause, Cockroach Community License (CCL), Dgraph (now using Cockroach Community License), Elastic License, Sourcegraph Fair SourceLicense, MariaDB Business Source License (BSL)… and many more.

The trend is toward “source-available” licensing rather than “open-source” licensing because source-available licenses, uncontaminated by the myopia of open source industry associations, do not require that Amazon have the “freedom” to take your code, run it as a commercial service and give nothing back to you.

To that end, a group of open-source lawyers led by Heather Meeker, a respected and undisputed leader on technology and open-source law who worked on both Commons Clause and SSPL, will soon open a suite of “source-available” licenses for community comment.

The suite of source-available licenses is expected to provide authors of open-source software with a number of methods to address the growing threat from cloud infrastructure providers. The suite will provide short plain-language source-available licenses; standardize patterns in recently adopted source-available licenses; and allow users and companies to mix and match limitations you want to impose (e.g. non-commercial use only, or value add only, or no SaaS use, or whatever else). I believe these frameworks will be a smart alternative to open source, as the OSI refuses to provide leadership in solving the Amazon problem.

More broadly, it is clear to most industry observers that AWS is using its market power to be anti-competitive. Unless something changes, calls for anti-trust action against both Amazon and AWS are inevitable, even if AWS is divested from Amazon. That issue is broader than just open source.

Amazon’s behavior toward open source is self-interested and rational.

Within open source, if Amazon isn’t breaking any laws today, then licenses to prevent or curb their behavior are critical. And lack of leadership from the open-source industry associations that squat on the term “open source” means that source-available licenses are the most viable solution to curb such behavior. It doesn’t have to be this way.

Leadership often comes from unexpected sources. There are promising signs that other cloud infrastructure providers are becoming true allies to the open-source community. Take Google, for example. The major announcements at Google Cloud Next in April 2019 were dramatic and encouraging. The company announced partnerships with Confluent, DataStax, Elastic, InfluxData, MongoDB, Neo4j and Redis Labs — companies most affected by Amazon’s behavior.

Google Cloud’s new CEO Thomas Kurian’s remarks echoed what I had been saying for the last year.

Frederic Lardinois of TechCrunch wrote:

Google is taking a very different approach to open source than some of its competitors, and especially AWS. … “The most important thing is that we believe that the platforms that win in the end are those that enable rather than destroy ecosystems. We really fundamentally believe that,” [Kurian] told me. “Any platform that wins in the end is always about fostering rather than shutting down an ecosystem. If you look at open-source companies, we think they work hard to build technology and enable developers to use it.”

It’s smart for Google to align with these commercial open-source players — AWS is beating Google in the cloud wars and giving best-of-breed commercial open-source products first-class status on Google’s cloud will help Google win more enterprise customers.

Perhaps more importantly, the stance and language on how ecosystems thrive is incredibly encouraging.

Disclosures: The author has invested in numerous open companies affected by the behavior of cloud infrastructure providers, indirectly owns shares of Amazon and, apart from any abuse of open source or anti-competitive behavior, is a big fan of Amazon.

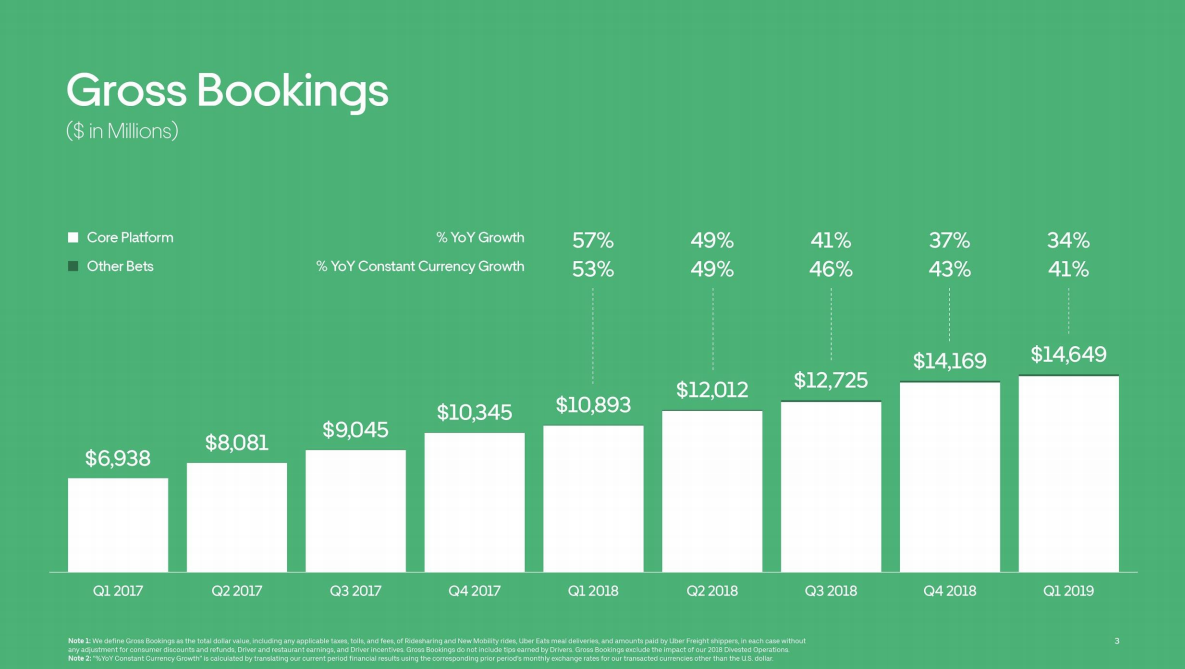

Uber’s ride-hailing business is growing more slowly than its newer bets. In Uber’s Q1 2019 earnings, the company reported gross bookings growth of 230% for its other bets, while ridesharing grew just 22% compared to the same quarter last year.

Gross bookings are the revenue earned minus things like taxes, tolls, fees, wages paid to drivers, restaurants and so forth.

Other bets, with gross bookings of $132 million for Q1 2019, includes freight and new mobility, which entails bikes and scooters. Uber did not break out specifics for new mobility, but Uber CEO Dara Khosrowshahi said on an investor conference call that gross bookings for new mobility “grew strong quarter over quarter.”

Meanwhile, Eats continues to be a revenue driver for Uber, with gross bookings growth of 108% to $3.07 billion.

Slowing growth of Uber’s core business is to be expected. At TC Disrupt last year, Khosrowshahi said ride-hailing will make up less than 50% of Uber’s business transactions.

faran follow

BLUETTI FridgePower review

Examining the ‘pipeline problem’

Easemate.ai review

I've tested a bunch of Shark vacuums and they all have the same problem

Axeleo Capital raises $51 million fund

Overwatch 2 is getting its first musical collab with K-pop girl group LE SSERAFIM

Oops! Intel just leaked its own Raptor Lake Refresh processors

Best website builder of 2019

Cybercriminals are targeting outdated WordPress sites to run phishing ads

faran follow

BLUETTI FridgePower review

Examining the ‘pipeline problem’

Easemate.ai review

I've tested a bunch of Shark vacuums and they all have the same problem

Axeleo Capital raises $51 million fund

Overwatch 2 is getting its first musical collab with K-pop girl group LE SSERAFIM

Oops! Intel just leaked its own Raptor Lake Refresh processors

Best website builder of 2019

Cybercriminals are targeting outdated WordPress sites to run phishing ads

0 coment�rios: